- Central bank decisions in the euro area, Canada and New Zealand

- ECB to watch – likely to signal rate cut in June

- In the US, the dollar will be driven by inflation statistics and Fed minutes

ECB Governing Council – time for interest rate cuts approaches

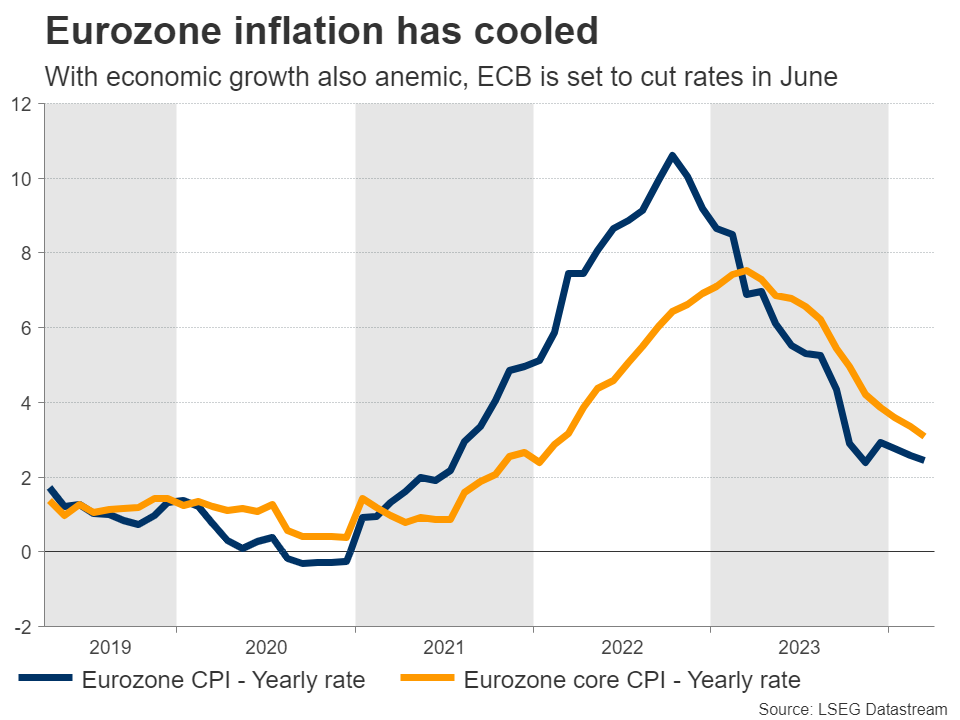

The euro area economy experienced difficult conditions last year. Economic growth has been largely stagnant, held back by Germany, as the slowdown in global trade has suppressed export demand and the domestic manufacturing industry has become dysfunctional.

On the bright side, economic stagnation is helping to contain inflationary pressures. Inflation fell to 2.4% in March, moving the European Central Bank one step closer to cutting interest rates. Most ECB officials point to a June interest rate cut as the most likely scenario.

Investors also share this view. June's interest rate cut is already fully priced into money markets, reflecting a slowing growth pulse and cooling inflation. The unemployment rate has also risen slightly this year, increasing expectations that inflation will start to decline.

The ECB is therefore likely to use Thursday's Governing Council meeting as a springboard to prepare for a summer rate cut. President Lagarde is likely to highlight the rise in inflation and argue that early interest rate cuts will help minimize the risk of a recession.

As for the euro, its bleak economic fundamentals paint a negative picture. One of the reasons the single currency has shown so much resilience over the past year is the decline in prices that has benefited the euro through trade channels. The euphoria in the stock market also contributed to pegging the safe-haven US dollar.

In other words, the euro has been sustained not by economic performance but by the development of other financial markets. TThis is a double-edged sword. This is because any change in these trends could mean that the currency could lose much of its support.

In other words, for the euro to stay above water, gas prices need to fall and stock markets need to rise. Otherwise, traders may start focusing on poor growth prospects and rate cuts.

Focus on US inflation and Fed minutes

In the US, all eyes will be on CPI inflation statistics and the latest Fed meeting minutes, both on Wednesday. These will help investors gauge whether the Fed will cut interest rates in June, with the market currently pegging the probability of that to be 70%.

Inflation is expected to accelerate again, with the CPI rate expected to reach 3.4% in March from 3.2% previously. However, core interest rates are expected to fall to 3.7%. The difference most likely reflects the rise in oil prices during the month, as the core numbers do not include the impact of energy prices.

This will result in a mixed report for the Fed. A decline in core interest rates would suggest that the broader disinflationary trend continues, even as headline inflation rises due to higher energy prices.

Meanwhile, the minutes will also address the March meeting, where FOMC officials revised their growth and inflation forecasts upward but still expect three interest rate cuts this year. It will be interesting to see the discussions behind the scenes. However, most officials have spoken several times since the meeting, so the latest announcement is unlikely to contain any groundbreaking revelations.

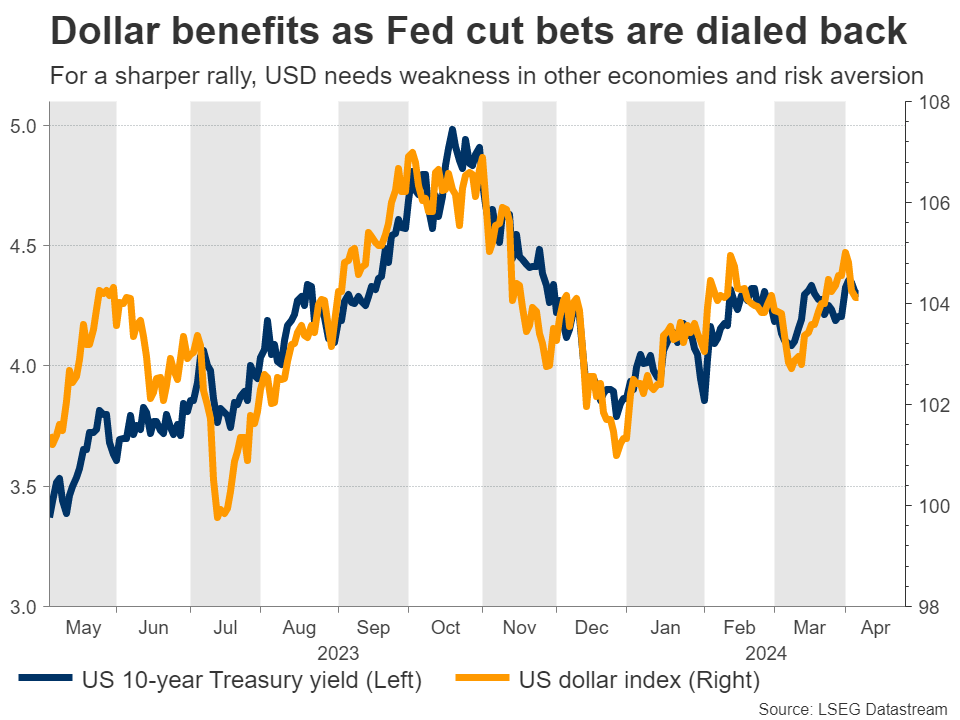

As for the dollar, it was volatile this week, stalling after a disappointing ISM services survey, but has since rebounded, helped by risk aversion due to concerns about an Iranian attack on Israel.

Overall, the fundamentals of the U.S. economy appear to be stronger than in other regions. For example, GDP growth is expected to reach 2.5% this quarter, according to the Atlanta Fed. Therefore, while further signs of weakness in overseas economies or a risk-off atmosphere to stimulate demand for haven assets may be needed for the reserve currency to see sustained gains, the broader outlook is positive. looks like.

Pricing in Canada and New Zealand

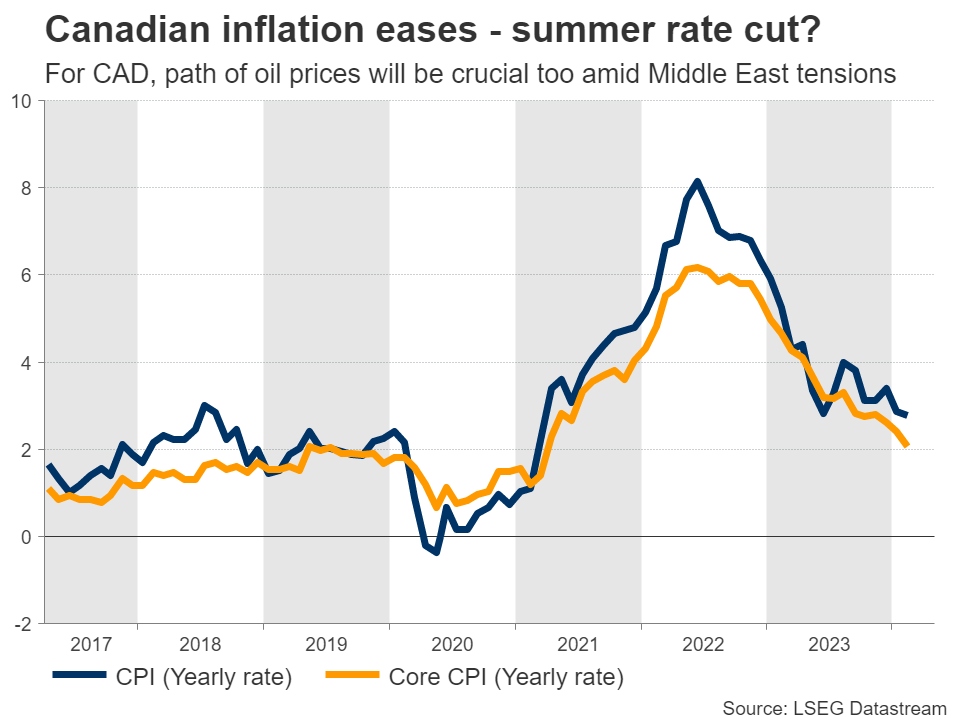

With core inflation steadily declining in Canada, the central bank meets on Wednesday and markets are pegging a 15% chance of an immediate rate cut. Significant population growth has eased labor market conditions and reduced concerns about wage-driven inflation. The downside is a housing shortage and continued shelter inflation.

So while the Bank of Canada is unlikely to cut rates at this meeting, it could give a clearer signal that a rate cut will occur this summer. The Canadian dollar is also driven by oil prices, and the escalating situation in the Middle East is likely to benefit the oil-exporting currency.

Entering New Zealand, the local currency has struggled this year, depreciating more than 4% against the US dollar. The economy entered a mini-technical recession late last year, weighing on consumer and business confidence. But with inflation remaining high, markets do not expect the Reserve Bank to take any action at Wednesday's meeting.

A sustained recovery in the New Zealand dollar will likely require a meaningful recovery that increases demand for China's commodity exports.

In this sense, all eyes will be on Friday to see if there are any signs of a rebound in China's trade data for March. Other notable announcements on Friday include the UK's monthly GDP statistics.