shareholders lost 72% on their investment in the stock 3 years ago")

Long-term investing is not possible without some degree of poor investment. But problems arise when you are faced with huge losses from time to time. So let's think for a moment about the following misfortune. Videndam (LON:VID) An investor held on to the stock for three years as the stock price fell by 75%. If that happens, our confidence in the decision to hold the stock will certainly be shaken. And the ride has been even less smooth lately compared to last year, when the price was 67% cheaper. Furthermore, about a quarter of them have fallen by 17%. That's not much fun for the holder.

Shareholders are down over the long term, so let's take a look at the underlying fundamentals over that time period to see if that's in line with the returns.

Check out our latest analysis for Videndum.

in his essay Graham & Doddsville SuperInvestors Warren Buffett explained that stock prices do not always rationally reflect the value of a company. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Bidendam has been profitable for the past five years. This is generally considered a positive, so we're surprised by the drop in the share price. So it might be worth checking out other metrics given the share price drop.

In fact, the share price decline doesn't seem to be driven by earnings either, as earnings are up 14% over three years. Perhaps Videndum is worth investigating further. This analysis may be missing something, but there may be an opportunity.

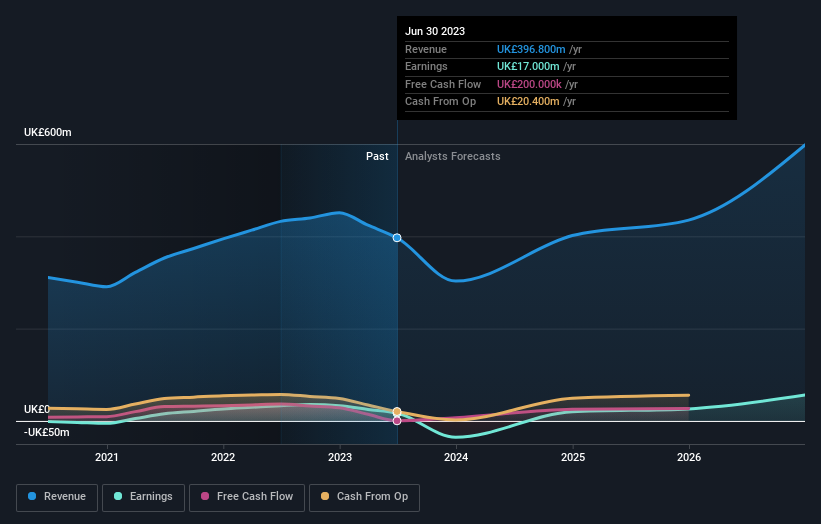

The company's earnings and revenue (long-term) are depicted in the image below (click to see the exact numbers).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide for a business.So I recommend checking this free Report showing consensus predictions

What about total shareholder return (TSR)?

We've already covered Bidendam's share price movement, but we should also mention its total shareholder return (TSR). The TSR seeks to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Videndum's TSR in his three years was a loss of 72%. Since it pays dividends, the stock price return wasn't too bad.

different perspective

While the broader market has gained about 6.7% in the last year, Bidendum shareholders have lost 66%. Even blue-chip stocks can see their share prices drop from time to time, and we like to see improvement in a company's fundamental metrics before we get too interested. Unfortunately, last year's performance ended on a down note, with shareholders facing a total annual loss of 11% over five years. I know Baron Rothschild said investors should “buy when there's blood on the streets,” but investors should first make sure they're buying a quality business. Warns you that you need to confirm. It's always interesting to track stock performance over the long term. However, to better understand Videndum, you need to consider many other factors.Case in point: we discovered 4 warning signs for Videndam You should know and two of them should not be ignored.

Bidendum isn't the only stock that insiders are buying.So take a look at this free A list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on UK exchanges.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.