(LON:GTLY) shareholders suffered a 15% loss on their investment in the stock 3 years ago")

To justify the effort of picking individual stocks, it's worth striving to beat returns from market index funds. However, any portfolio may have some stocks that underperform its benchmark.I regret that it has been a long time since I last reported. Gateley (Holdings) Plc (LON:GTLY) shareholders have had their share of the experience, with the share price down 28% over three years, compared to a market return of around 18%. Recent news that the stock price has fallen 27% in one year is not very reassuring. The decline has accelerated recently, with shares down 20% in the past three months.

So let's take a look at whether the company's long-term performance is in line with the progress of its underlying business.

Check out our latest analysis for Gateley (Holdings).

Markets are powerful pricing mechanisms, but stock prices reflect not only underlying business performance but also investor sentiment. One way he looks at how market sentiment has changed over time is to look at the interaction between a company's stock price and his earnings per share (EPS).

During three years of an unfortunate share price decline, Gateley (Holdings) actually improved its earnings per share (EPS) by 0.1% per year. Given the stock price reaction, one might suspect that EPS is not a good indicator of performance during the period (perhaps due to temporary losses or gains). Alternatively, the company was overhyped in the past and its growth disappointed.

Considering this number, we think the market had higher expectations for EPS growth three years ago. However, looking at other business metrics may shed a little more light on the share price movement.

Given the health of its dividend payments, I don't think that caused any concern to the market. It's good to see that Gateley (Holdings) has grown its earnings over the past three years. However, it is not clear why the stock price is falling. It might be worth digging deeper into the basics to make sure you don't miss out.

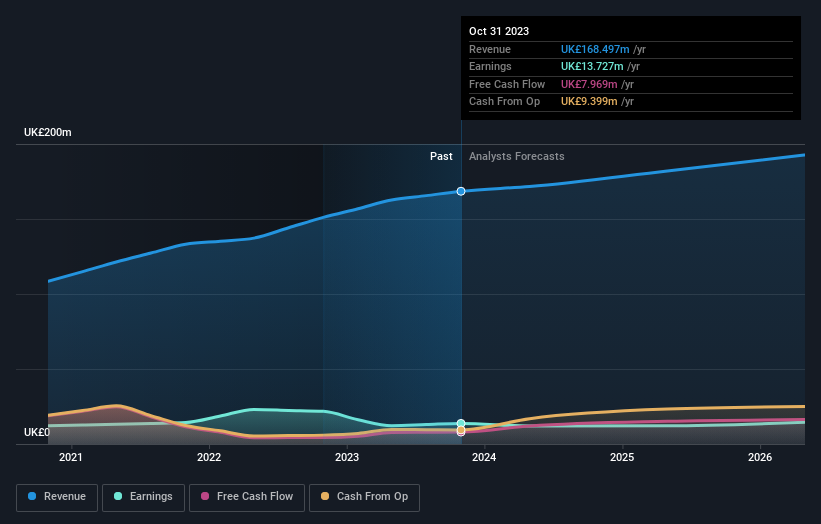

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We're pleased to report that our CEO is paid more modestly than most CEOs at similarly capitalized companies. While it's always worth keeping an eye on CEO pay, the more important question is whether the company will grow its earnings over the years. You can see what analysts are predicting for his Gateley (Holdings) in this article. interaction Graph of future profit forecast.

What will happen to the dividend?

As well as measuring share price return, investors should also consider total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often much higher than the share price return. We note that Gateley (Holdings)'s TSR over the last three years was -15%, which is better than the share price return mentioned above. This is primarily due to dividend payments.

different perspective

Investors in Gateley (Holdings) have had a tough year, losing a total of 22% (including dividends) versus a market gain of around 6.1%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. On the bright side, long-term shareholders have made money, with a return of 0.7% per year over 50 years. If fundamental data continues to point to long-term sustainable growth, the current selloff could be an opportunity worth considering. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. To do so, you need to know the following: 4 warning signs We worked with Gateley (Holdings) to investigate.

For people who like searching succeed in investing this free This list of growing companies with recent insider purchasing may be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on UK exchanges.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.