As part of Morningstar's Special Report Week on Thematic Investing, we take a look at the clean energy stocks that have underperformed since 2020 and the outlook for the broader renewable energy industry.

The energy crisis sparked by the Ukraine war, combined with broader demands to combat climate change and decarbonize the economy, has led to an unusual surge in investment in renewable energy, particularly in Europe.

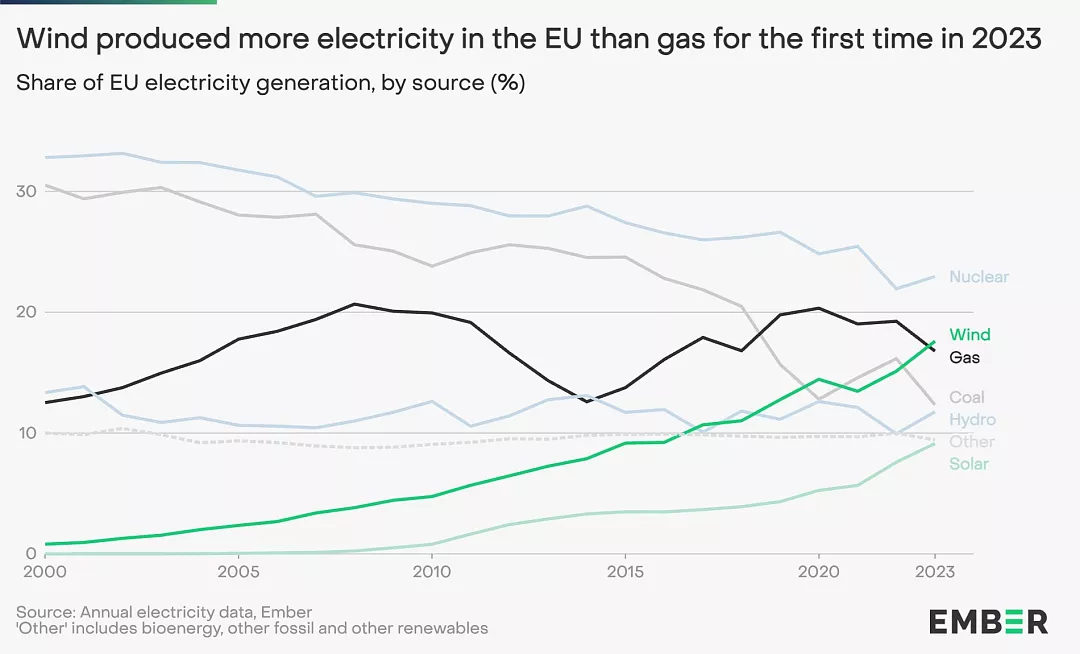

Much has been achieved on the supply side over the past two years. In 2023, wind power will exceed fossil gas for the first time in Europe's electricity supply, according to statistics from think tank Ember. Last year, wind and solar power generated 27% of the EU's electricity, a record high. Coal and gas declined as well, with the former falling to an all-time low of just 12% of EU electricity production.

“Europe's energy sector is undergoing significant change,” says Sarah Brown, Ember's European program director. “While fossil fuels play a more important role than ever before, systems with wind and solar backbones are emerging.”

However, the average Morningstar Category return for sector equity alternative energy funds (which also includes ETFs) was -11% in 2022, -10.5% in 2023, and -4.3% year-to-date (figures are in euros, current ) April 15, 2024).

There are also some funds within this group that have performed much better, especially in 2023, such as Pictet Clean Energy Transition and Robeco SAM Smart Energy Equity, all of which are actively managed. .

Energy projects struggle with high interest rates

There are four factors that have had a particularly negative impact over the past year. Rising interest rates leading to higher costs of capital, high inflation leading to higher development costs, network bottlenecks and finally supply chain difficulties.

“Overcapacity is the most important driver of this prolonged downturn, as supply is more than adequate for current demand,” said Fabrizio Arrusa, senior relationship manager and ETF specialist at Invesco. . “While this is an advantage, it does put pressure on margins. Competitive pricing compared to fossil fuels is a big part of what makes this strategy viable for climate change.”

“Factors such as rising interest rates particularly impact renewable energy companies due to the long-term nature of their cash flows and leveraged assets. Additionally, offshore wind projects, particularly in the United States, face increased risks. “There are several projects,'' explains Manuel Rosa, Senior Portfolio Manager at the Pictet Clean Energy Transition Fund.

Clean energy projects have high initial costs and are highly sensitive to interest rates.

“To name a few numbers: [power] The life cycle of a plant is typically around 30 years, with the first 10 to 15 years being contracted. However, in many cases it is financed with debt whose average maturity is 7 years. “Existing assets that were developed and financed during periods of low interest rates are now more difficult to finance in the current environment, creating a challenging situation for power producers with existing operational projects.” said Aanand Venkatramanan, head of ETF EMEA at LGIM.

“However, it is important to remember that the transition to clean energy is not just limited to renewable energy. Sectors such as semiconductors, green buildings, power grids and electric vehicles also play an important role.” Pictet says Rosa. And indeed, the Swiss fund manager's 2023 strategy was able to outperform the MSCI ACWI index, primarily due to its higher exposure to these sectors.

Investment and the Greenium Effect

Passive investments, on the other hand, have struggled even more, with the most high-profile victim of weather changes being the iShares Global Clean Energy UCITS ETF USD (INRG). The fund was an absolute top performer in 2020, but has lost about 43% of its value since January 2021.

“Although the S&P Global Clean Energy Index has struggled, the clean energy sector includes a wide range of stocks, so it is important to distinguish between: pure playerWe focus solely on clean technology and the rest of the world, including renewable energy, utilities and green industries,” explains Natalia Luna, Senior Thematic Investment Analyst at Columbia Threadneedle Investments.

“In this sense, a sharp decline Pure thematic playerIt has benefited from high ratings. greenium “This is an effect of investors' willingness to pay a premium for sustainability in an environment where enthusiasm for ESG issues drives significant capital inflows,” Luna continues.

“In fact, many companies experienced negative profitability and a natural correction in the face of a more difficult macroeconomic environment that resulted in a reversal of ESG inflows.”

Another important development is that consumer prices for renewable energy have fallen significantly over the past two years, even though production costs have increased significantly over the same period, putting strong pressure on companies' margins. That's the fact.

Powering Clean Energy: Low Rates, Cheap Inventory

Valuations of clean energy stocks experienced a real boom in the immediate aftermath of the first wave of the coronavirus. LGIM's Venkatramanan said, “These valuations reflect over-optimism regarding project fundamentals and the macroeconomic environment.”

But since then, the value of those stocks has fallen significantly.

“We believe that the market assessed the renewable energy sector too negatively in 2023, adopting a general approach that neither captured the sector's structural support factors nor differentiated between different players. ” explains Natalia Luna. “Nonetheless, our investment approach to the energy transition remains unchanged and we continue to forecast positive and sustained growth, although not without hurdles related to the timing of the permitting process and the challenges associated with the energy transition.” doing” supply chain and increasing bottlenecks within the power grid. ”

For Invesco's Alusa, current valuations for the investment universe are “very attractive” so far. Additionally, it's an election year for U.S. markets, and a Democratic victory is “likely to be a boon for clean energy stocks.”

Roman Bonner, senior portfolio manager at RobecoSAM Smart Energy Equity Strategy, said: “The sharp rise in interest rates could provide much-needed valuation support to the renewable energy sector, which has been negatively impacted by rapid increases. “It will become,” he says.

“We believe the current rise in capital costs is only a temporary setback for the renewable energy sector, as growth prospects for this decade remain strong and financing remains widely available. This creates an attractive entry point in the medium to long term. This is a long-term structural issue that will follow a non-linear path with winners and losers.”

Overall, Bonner and Robeco's management believe that even in the face of a more difficult macro scenario, “higher energy prices and the urgent need for energy independence will act as a catalyst for increased investment in smart energy.” “We are confident in our earnings outlook for 2024.” technology. ”

AI and clean energy

Not only geopolitical issues, but also the future of technology is pushing us towards cleaner and cheaper sources of power. “In fact, it is estimated that the demand for electricity driven by AI (artificial intelligence) will reach the current level of demand across Europe within a few years,” says Manuel Rosa.

According to Rosa, the energy transition of our economy will undergo three fundamental changes. The second is widespread electrification, starting with areas such as transportation and building heating. The last one is about improving energy efficiency. The need to reduce energy usage and increase optimization is becoming increasingly important. ”

“The increasing efficiency of renewable energy and the falling price of electric vehicles will certainly continue to drive this trend,” says the Pictet manager. It's a policy intervention. ”